Here’s a scenario that plays out in small businesses every single day:

- You closed a great month.

- Sales are up

- Clients are happy

- Your P&L looks solid.

Then Friday hits, and you’re staring at your bank account, wondering how you’re going to make payroll.

Sound familiar? You’re not alone. It’s not that you’re not bad at business. It’s just that you haven’t yet mastered cash flow. There’s a difference between being profitable on paper and actually having cash available to run your business. That gap is one of the leading causes of business failures, so let’s fix it!

First, Understand What You’re Actually Dealing With

The cash flow statement includes three distinct “personalities”, described as:

Operating cash flow is the money you use day to day. Cash generated from selling your product or service.

Investing cash flow shows what you spend or receive from buying or selling long-term assets, such as equipment.

Financing cash flow is cash from external sources, such as loans, owner withdrawals, or investor funds.

The most common mistake business owners make is confusing cash with profit.

You can invoice $50,000 this month and have $0 in the bank if nobody’s paid you yet. This situation is commonly known as a cash-flow crunch.

NOTE: While a typical coffee shop won’t usually run into problems if it’s cash-only, if the owner also offers catering, they’re likely to accept credit from customers. That is the situation in this scenario!

The two numbers you need to understand right now: your working capital (current assets minus current liabilities) and your burn rate (how fast you’re spending cash). If your burn rate exceeds your cash inflows, your business is on borrowed time.

You Can’t Fix What You Don’t Measure

Most business owners check their bank balance and call it “monitoring cash flow.” That’s like checking whether your car has gas by looking at the dashboard. While useful, it’s not the complete picture.

Real monitoring means using a cash flow statement (what actually moved) and a forecast (what’s coming).

Here’s how:

Start by listing all your expected cash inflows (like customer payments) and outflows (bills, payroll, rent) for each of the next 13 weeks.

Use your calendar and past payment habits to help estimate these numbers. Every week, compare actual results to your forecast and adjust next week’s forecast as needed. This process gives you a clear view of upcoming shortfalls or surpluses, so you can plan ahead. It may seem boring until it saves your business.

Add historical trend analysis to spot your own patterns. Does revenue tank every January? Does Q3 crush it? Your history can be insightful.

Track your financial ratios:

- The current ratio helps you determine your ability to pay short-term bills and is calculated by dividing current assets by current liabilities.

- The quick ratio shows if you can pay off current liabilities without selling inventory. The quick ratio is calculated by summing the current assets that can be converted to cash quickly (cash, marketable securities, and accounts receivable). Then, divide that total by liabilities.

- Your profit margins show how much money you keep after costs.

These aren’t just banker metrics. They are crucial to the sustainability of your business.

Tools like QuickBooks or Xero make this dramatically easier, and if you’re growing, a virtual CFO or financial dashboard can give you real-time visibility without the full-time salary.

Get Paid Faster. It’s That Simple (And That Hard)

To improve cash flow quickly, focus on speeding up incoming payments, not on cutting costs. While cutting costs can help in the short term, it is not sustainable for business growth.

Fastrack invoicing means that the moment a job is completed or a milestone is reached, the invoice goes out. Make it a priority. Every day of delay is a day you’re giving your client an interest-free loan at the expense of your business.

Want to incentivize faster payment? Try early payment discounts. You can offer something like 2% off if they pay within 10 days instead of 30 (written as “2/10 Net 30”). Most clients will take that deal, and you’ll be amazed at how much it improves your cash position.

For larger projects, never start without a deposit. Structure billing around milestones. You finish phase one, you get paid for phase one. Depending on the advice of your lawyer, you may be able to structure your contract with this understanding of milestone payments. Further, this is standard in most industries, so don’t be afraid to ask.

Make it stupidly easy to pay you. Accept credit cards and online payments. Yes, there’s a processing fee. It’s worth it. Every friction point in your payment process costs you days.

Tactfully work with clients who consistently make late payments. Don’t let overdue accounts sit and age. And if you want truly predictable cash flow, explore recurring revenue models in which clients pay upfront each month.

For businesses with large receivables (money owed by customers), factoring means selling your invoices to a third party for immediate cash. This is a legitimate option when you need liquidity (readily available money) fast.

Pay Slowly but Ethically, Legally, and Strategically

This is the mirror image of collecting fast: when it comes to paying your bills, there’s no prize for being early.

Start by negotiating extended terms with your vendors. Most vendors quote net 30 days, but you can request Net 45 or longer. Vendors will likely work with you because they want your business, especially if you’re a reliable customer. You’d be surprised how rarely people ask. Try to make those extended payments on time, or your vendors will become less accommodating.

Use credit cards for your operating expenses and pay them off monthly. That’s an automatic 30-day float. This time period can help your business wait to collect money from your customers. Don’t overuse this, though. Extending it beyond the float will trigger higher interest rates, which eat into your profits.

Lease equipment instead of buying when possible. Your cash flow will thank you. Ownership is great for your ego; leasing is great for your bank account.

Pick scheduled set payment days. For instance, suppose you decide that every Monday is your day to pay bills, rather than paying them as soon as they arrive. This batches your outflows and gives you better visibility into your weekly position. Choose any day of the week that makes sense for you, though. It doesn’t have to be Mondays.

Audit your subscriptions. Every business has them. That $47/month tool nobody uses, the software you replaced six months ago but forgot to cancel. Cut all unused subscriptions immediately. There are services that can do this for you, as well.

Don’t fall behind on inventory tracking. Excess stock is cash sitting on a shelf. Auditing regularly can unlock thousands of dollars you didn’t know you had.

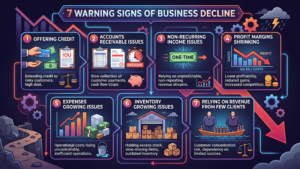

The Mistakes That Will Quietly Bankrupt You

Mixing personal and business finances is the number one cash flow killer for small business owners. The moment you run personal expenses through your business account (or vice versa), you lose visibility into both. Separate everything. Now.

Related to this: having a single bank account muddies everything. You don’t actually know how much money you have for operations, taxes, or profit because it’s all lumped together.

100% delegation without oversight is a trap. Hire a bookkeeper or accountant, but review the numbers yourself. Fraud and errors happen. Your job isn’t doing the bookkeeping; it’s understanding what the numbers say.

Watch out for overestimating sales while underestimating costs. Be conservative in your forecasts. If you hit your optimistic number, great. But build your cash plan around a realistic (or even pessimistic) scenario.

And if your business is struggling, don’t use loans to cover survival expenses. These loans become unserviceable, meaning the business cannot repay them from its own cash flow, forcing you to keep borrowing just to survive. Strive for serviceable debt instead. Serviceable debt helps businesses grow and pays for itself. Survival debt just deepens the hole.

Build a Financial Reserve Before You Need One

Emergency funds aren’t just for personal finance. Your business needs 3 months of operating expenses in a reserve account. Period. If that feels impossible right now, start with one month and build from there.

Open a business line of credit while your business is healthy. Banks lend umbrellas when the sun is shining and take them back when it rains. Don’t wait until you desperately need it.

For your reserve funds (money set aside for emergencies), don’t let them sit idle. CD (certificate of deposit) ladders and money market accounts (types of accounts that earn interest) let you earn something while keeping the cash accessible. It’s not exciting, but neither is watching cash evaporate with nothing to show for it.

If you need a capital injection, know your options: asset sales (do you have equipment or IP you’re not using?), equity investment through crowdfunding or angel investors, or good old friends-and-family loans, structured properly with real terms in writing.

Level Up: The Advanced Moves

Once you’ve got the basics locked in, the following strategies may help you grow your business and move beyond survival mode.

Build a variable-cost model, so your expenses naturally scale with revenue. If a slow month hits, your costs go down too, rather than leaving you holding fixed overhead you can’t cover.

If your business is seasonal, plan for it proactively. Save aggressively in peak months. Build that Q3 war chest so Q1 doesn’t blindside you.

Set aside 25–30% of profits for taxes from day one. Remember the old adage that there are two certainties in life: death and taxes. None of us can do anything about the first one. But we can try to prepare ourselves for tax events.

Finally, invest in your own financial literacy. You don’t need to become an accountant. But you do need to understand your numbers well enough to ask the right questions, catch problems early, and make smart decisions. An hour a week reviewing your financials will pay for itself a hundred times over.

Cash flow management isn’t glamorous. It doesn’t give you the same dopamine rush as a new sale or customer. But cash flow management is foundational, and over the long run, keeping your business running smoothly and helping it manage the trickier aspects of running a business will bring its own satisfaction.

Start with one thing from this list. Just one. Then add another. When you turn these items into habits, they become part of your business flow.

Your business deserves to stay alive long enough to reach its potential. Don’t let a solvable cash problem be the reason it doesn’t.

Be First to Comment