I remember learning about covered calls about 20 years ago. I was reading about them in an investing rag that I subscribed to at the time. They touted it as a low-risk strategy, and in the context of options investing, the framing is largely correct.

The site owner may receive a commission on sales made through the links on this page.

It’s important to understand that covered calls are not riskless. They are simply less risky than writing naked calls, which have theoretically unlimited risk. I’ll do a quick overview of all these terms, as understanding them is necessary to understand why covered call ETFs can be covertly risky.

Let’s start with the most basic definition in options investing: the call option. NOTE: I won’t be discussing put options as doing so would muddy the waters of this discussion. A simple Google search will show plenty of articles and posts covering both calls and puts.

In options investing, a call (a contract) gives the holder the right, but not the obligation, to purchase shares of a stock at an agreed-upon price on an agreed-upon date. Most stock options trade in contracts that control 100 shares. If you were to buy a call option on Microsoft, you would be given the right to purchase 100 shares of Microsoft. Two contracts would allow you to purchase 200 shares.

In options parlance, the agreed-upon price is the strike price. The underlying is the company you are buying the contract for (Microsoft in the above example); the agreed-upon date is the expiration date. And the premium is the amount you pay to hold that option for the duration of the contract.

Another important definition concerns whether a contract is naked or covered. A naked option essentially exposes the seller to potentially unlimited risk (assuming the stock could increase in price infinitely).

A covered call, on the other hand, limits risk but also limits the upside potential of the stock appreciation, and this is the cornerstone of covered call risk, as will be explained in this article.

When you own 100 shares of stock (or multiples of 100), if you ask to enable options trading in your account, you may create a contract on the options exchanges (called writing an option) to give the option contract buyer the right, but not the obligation, to purchase 100 shares of the stock you own. For this right, you are paid a premium.

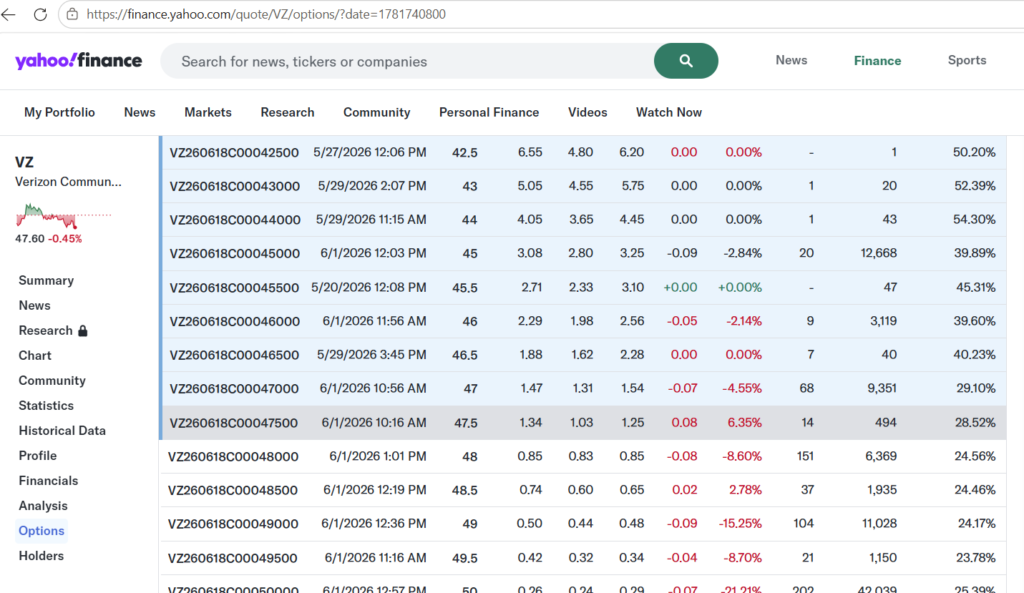

Verizon Example

Let’s say back on May 15, you bought 100 shares of $VZ at 46 (the price closed at 46.37, but you got a good fill earlier). Here is the Stock Analysis screen showing the prices.

On May 29, you decide you want to write a call on your 100 shares of Verizon. As you can see from the Stock Analysis data, the stock price fluctuated between $47.34 and $ 48.16 that day.

There are many strike prices that you can choose from, as well as expiration dates. You can find option pricing on Yahoo Finance. Covered call writers try to find the shortest possible expiration date that gives them a decent premium. Premiums usually increase as you go further out in time, but that means you are tying up your capital for that duration as well.

For this example, I chose June 18th for the expiration date and chose $47.5 as the strike price because it is close to the underlying’s price (this is called at the money – I will have links to all definitions in the resources).

On 5/29, the at-the-money strike price of $47.5 closed at $1.26. Remember that options contracts are for 100 shares, so the premium would be $126.

If you are a covered call writer, you get to keep that premium no matter what happens to the stock. The ultimate goal for covered call writers is for the stock to stall out in price. If the price jumps, your call will be exercised, and you will have to sell your $VZ stock at $ 47.50 (x 100). Now, you could still be happy with this because you bought the stock at $46 and sold it at $ 47.50, for a $ 1.50 gain. Plus, you collected a premium of $126. So overall, you made $150 + $ 126, for a total of $276.

However, if the price jumps to $60 during the contract, you still gain with the $276, but you lose out on any appreciation after the stock passes $47.5. For the $60 scenario, that difference is just over $11 per share, or $1,100. If the stock price had gone to $79, the opportunity cost would have been slightly over $3,000.

This example illustrates the first risk of covered calls: the opportunity cost. While you didn’t lose any money and actually gained a little ($276), the $1,100 (stock price went to $60) or $3,000 (stock price went to $79).

Opportunity risk is at the heart of NAV erosion in covered call ETFs. It’s not easy to track without actually running the numbers. Doing so would require knowing what trades the ETFs make.

The second scenario is the sweet spot for covered calls. The stock remains below the strike price but above (or at least at) the purchase price. The covered call expires, and you keep the premium. You can now write another covered call and collect even more premium.

The third scenario is that the stock falls significantly. Your covered write will expire worthless, but your shares are now worth less as well. You, as an individual investor, have no obligation to write another covered call on your stock at a lower price.

However, a covered call ETF is often required to do so because that is the strategy they defined for themselves during the prospectus period. So if $VZ dropped to $35, the ETF would likely have to abide by its binding investment mandate and write a covered call on or close the $35 strike, even though it paid $46 for it.

Cash Settlement, Notional Values and Synthetic Trades

Here we go with more terminology and jargon, right? I would normally avoid using these terms, but if you seek information from chatbots or elsewhere, they are likely to confuse the conversation by using them in their definitions. It’s technically not their fault as they are correct in their presentation. But it definitely makes it more difficult, something that, in my opinion, should be explained easily. That is the motivation for this article.

Be prepared because this gets a bit wonky, but I will try my best to explain it.

When I worked on trading desks, I was a data analyst at a fixed-income derivatives bank. At the time, I didn’t understand a lot of the jargon being bandied about by the traders. I did have a few traders willing to explain concepts, and one in particular struck a chord with me: synthetic trades and replication.

Traders often create models using synthetic trades (which use financial derivatives to replicate the risk and payoffs). Essentially, these synthetic positions act similarly (theoretically) because they share the same risk profile. So they should be priced the same. If they are not, there would be computerized arbitrage, which would align the value of the trades within milliseconds. As a result, arbitrage is not really an issue with these methods because it occurs so quickly that it is effectively nonexistent.

Given what was just explained, this allows for settlement in cash, as if the non-synthetic real trade had been executed. For covered calls, there would be no actual exercises. It would be as if there were an exercise from a cash perspective, followed by the repurchase of new shares to satisfy the mandate discussed earlier. Except there would be no repurchase either. They would just keep using the synthetic position to keep synthetically covered calls open.

They often use notional values (the as-if traded values) on instruments like ETNs (which are unsecured debt instruments issued by banks that track an index or benchmark – there is also counterparty risk, too) to structure the trades in a way that matches actually going through the motions and writing covered calls, exercising them (which requires selling the underlying), and then repurchasing new underlying stocks at whatever the price is marked at the time.

Pulling It All Together – How It Leads to NAV Erosion

Now that you know the complicated way to explain this (which is needed because technically, it is how these work), I will continue with the real trades. But just know that most of these covered call ETFs are implemented using the synthetic methods I described. You just have to think in terms of a kind of equivalency to them.

An ETF manager buys 100 shares of a stock at $20 a share for a total of $2,000 (we’ll stick to one stock – it’s often several and more shares). The stock rises to $25, and the manager sells 1 covered call contract for $2. At expiration, the stock is $30. The covered call is exercised:

Stock bought at $20

Covered Call written for a strike price of $25, premium = $2 per share = $200

Stock sold (due to exercise) at $25

Profit on stock: $5 per share x 100 = $500

The ETF’s total cash on hand: $2700 (original purchase) + $700 profit (from stock sale and call premium)

Here is where the NAV erosion occurs. Due to the prospectus mandate, the ETF must now purchase 100 shares at the new price of $30, or $3,000. But the ETF only has $2,700, the $2,500 from the exercised sale plus the $200 premium. That $300 shortfall is the direct result of having capped the upside at $25 while the stock ran to $30.

Hopefully, I explained this in a way that helps you grasp the risk of covered call ETFs. I am not telling you any of this to sway your decision. It’s just good to know the risks of the investments you are making.

[…] Covered Call ETFs May Be Paying You with Your Own Money […]