ETFs allow you to buy a single fund, which gives you instantly a slice of hundreds, sometimes thousands, of companies. You get diversification, low costs, and almost no maintenance. That convenience is one of the best financial innovations of the last fifty years, and it helps explain why ETFs have come to dominate the market.

But there is a more subtle side to this story, one that rarely comes up at the dinner table or in the financial news. When you invest through an ETF, you typically give up your voting rights in the companies you own. That tradeoff is the hidden cost this piece is about.

At first glance, that doesn’t sound like much of a sacrifice. How much influence could your twenty-five shares of Apple really carry at a shareholder meeting? Probably none. You’d be right to shrug it off.

But here’s the part that doesn’t get talked about enough: when millions of investors shrug it off at the same time, the voting power they’re giving up doesn’t vanish. It gets handed to someone else, adding up to something enormous that changes who has influence. That’s where the real stakes begin.

A Simple Example

Say you own shares in a fund that tracks the S&P 500. In your head, you might think of it simply: I own Microsoft. I own Apple. I own Nvidia. And in an economic sense, you’re right. You share in the gains and the losses. You collect your portion of the dividends. You benefit when the businesses you’ve invested in grow.

But when one of those companies holds its annual shareholder meeting and puts a vote to the floor, you are almost never the one filling out the ballot. The fund company is. Instead of millions of individual investors casting their own votes, a small number of asset managers vote on their behalf, all at once, as a block.

That distinction sounds technical, but it changes who actually has a say in how some of the world’s largest companies are run, and that is the core issue: ETF investing can separate economic ownership from voting power.

Why Corporate Voting Exists in the First Place

To see why this matters, let’s explore why shareholders get a vote at all.

When you buy stock in a company, you become a partial owner of it. And ownership comes with a voice in how the business is governed. Shareholders are typically asked to weigh in on board of director elections, executive pay packages, major mergers and acquisitions, and various governance proposals.

In theory, this is a system of checks and balances. Management runs the company day-to-day, and shareholders oversee management from a distance, with the power to vote out directors or block decisions they believe are reckless. It is one of the few real levers an owner has if they believe a company is heading in the wrong direction. Strip away the vote, and ownership becomes more passive. You still get the economics, the dividends, and the price appreciation, but you lose the part of ownership that lets you actually push back.

Why This Matters More Than People Tend to Think

Most people pay far more attention to political elections than they ever will to a corporate proxy vote, and that makes sense. Tax policy, regulation, and government spending touch daily life in obvious ways.

But corporate boards make decisions that move trillions of dollars through the economy each year, decisions about hiring, capital spending, acquisitions, product strategy, dividends, buybacks, and how much the CEO gets paid. Those choices ripple out to employees, customers, suppliers, and communities well beyond the shareholders who technically cast the votes.

This isn’t a fringe academic concern, either. It has become an actual fight playing out in real time among the largest fund managers in the country, which is exactly why it’s worth understanding.

How Concentrated the Voting Power Has Actually Become

Here’s where the numbers matter, because the scale of this is genuinely surprising. Harvard Law professor Lucian Bebchuk and Boston University’s Scott Hirst have spent years tracking exactly how much voting power has shifted to the largest index fund managers, BlackRock, Vanguard, and State Street, often called the “Big Three.” Their research found that as of the early 2020s, the Big Three collectively cast a median of roughly 27.6% of the votes at S&P 500 annual meetings, with BlackRock and Vanguard alone each holding close to a tenth or more of the votes at a typical company.

That share is not standing still. The Big Three have nearly quadrupled their collective ownership stake in S&P 500 companies over the past two decades, and each now holds 5% or more of the shares in many public companies. Extrapolating from that trend, the same researchers estimate that the three firms could be casting as much as 40% of the votes at S&P 500 companies within two decades.”

To be clear, holding a quarter or more of the votes at a company doesn’t mean a fund manager controls it outright. Corporate governance is messier than that, and plenty of other shareholders, executives, and board members are part of the picture too. But when one of three firms can swing the outcome of a close vote at thousands of companies simultaneously, the basic question is no longer whether ETFs are convenient. It is who should hold the vote that convenience leaves behind.

Asset Managers Are Starting to Hand Some of the Vote Back

This is the part of the story that’s changing fastest, and it’s worth knowing about if you’re an ETF investor wondering whether you’re stuck with this tradeoff forever. The broader question is whether investors can keep the convenience of ETFs without permanently surrendering the vote.

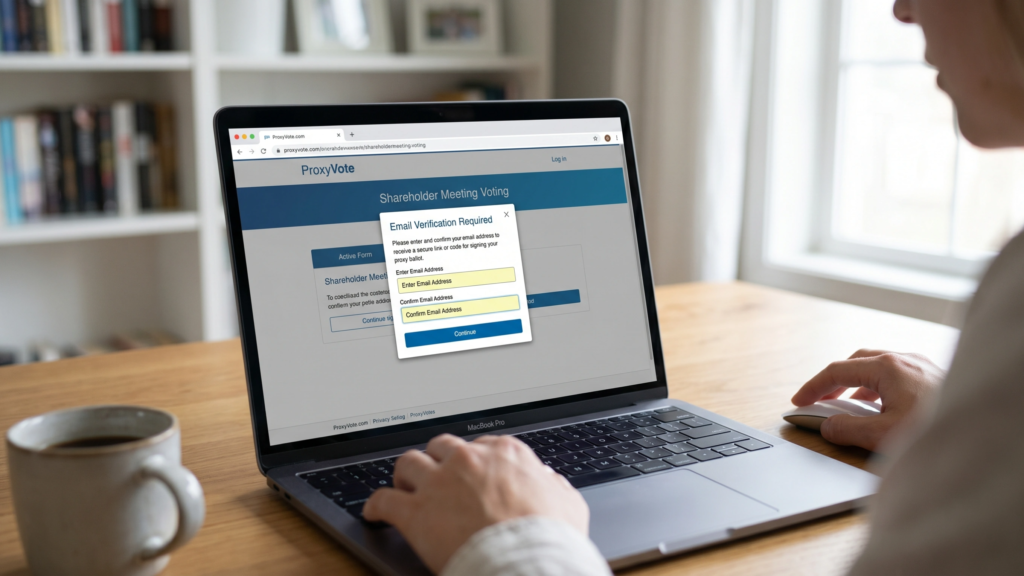

In the past few years, the major fund managers have rolled out what’s known as pass-through voting, letting individual fund holders choose how their slice of the vote gets cast rather than leaving every decision to the house policy. Vanguard’s version is called Investor Choice, and as of 2026, it covers 32 of its funds, including the flagship 500 Index Fund, reaching roughly 22 million eligible investors and nearly $4 trillion in assets.

Vanguard has also made it easier to sign up, partnering with Broadridge in 2026 so that investors who hold Vanguard funds through outside brokerages can select a voting policy on ProxyVote.com using just their email address, instead of needing a Vanguard account.

BlackRock runs a similar program called Voting Choice, first launched in 2022. It currently lets eligible clients select from seven third-party proxy voting policies, in addition to BlackRock’s own benchmark guidelines, with the chosen policy applied to a client’s proportional share of the fund. As of early 2026, index equity clients representing roughly $851 billion in assets were actively using the program.

These programs are still far from universal. Plenty of popular ETFs aren’t covered yet, and the sign-up process isn’t always obvious unless you look for it. But the direction is clear: the asset managers that built their businesses on holding your vote for you are now under enough pressure, partly regulatory and partly reputational, that they’re starting to let you take some of it back. If you want to know whether your specific fund offers this, it’s worth checking the fund provider’s website directly, since coverage is expanding on a fund-by-fund basis.

The Collective Action Problem

Even with these new options, most investors still won’t opt in, and that gets at something deeper than just ETF mechanics. It’s a classic collective action problem. Each individual investor correctly figures that their one vote barely matters, so they don’t bother. Multiply that reasoning by tens of millions of people, and you get a predictable result: almost nobody participates directly, and the voting power that was once scattered thinly across the population concentrates in the hands of a few firms by default.

This isn’t unique to ETFs. It’s the same logic behind low turnout in local elections or homeowners’ association votes. What makes the ETF version distinctive is that most investors aren’t even abstaining. They often don’t realize there was a vote to abstain from in the first place.

So What Do the Big Three Actually Do With All That Power?

This is the question that actually matters for deciding whether any of this should bother you. The point is not just who votes, but what ETF investing changes about ownership itself.

The honest answer is that the Big Three have historically been criticized for being too passive, not too aggressive. Bebchuk and Hirst’s research found that, despite their outsized voting power, the Big Three spend strikingly little on stewardship relative to the size of their holdings and, as of a few years ago, had no direct engagement with roughly 90% of their portfolio companies in a given year, on average.

Critics on one side argue that this passivity lets management teams coast without real accountability. Critics on the other side argue the opposite problem: that when the Big Three do engage, their house-voting policies on issues like board diversity and climate disclosure end up imposing one firm’s preferences on thousands of companies and millions of investors who never weighed in.

That tension has shown up directly in how the policies have shifted. Heading into the 2026 proxy season, both BlackRock and Vanguard softened their stances on several fronts, pulling back from personal-characteristic-based diversity considerations in board assessments and moving toward more general, less prescriptive, case-by-case language across multiple governance topics.

Whether you read that as a healthy correction or a worrying retreat probably depends on what you wanted those votes to accomplish in the first place, which is exactly the point. A small number of firms making that call for everyone is the whole issue in miniature, and it shows why the payoff of the debate is so significant.

Should Any of This Stop You From Buying ETFs? The answer depends on whether you think convenience is worth giving up the vote.

No, not really. ETFs remain one of the most useful tools investing has ever produced, and for most people, the benefits of broad, low-cost diversification still outweigh the loss of a direct vote they were unlikely to cast anyway. The point of all this isn’t that ETFs are a bad deal. It’s that every investment choice comes with tradeoffs, and this is one that rarely gets named out loud.

Why Individual Stocks Still Have a Place

Over the last decade or so, some investors have started treating individual stock picking like a relic, something only hobbyists or stubborn traditionalists still bother with. The logic is understandable. Why spend hours researching one company when a single ETF gets you exposure to hundreds?

But owning individual stocks still gives you something an ETF doesn’t: a direct line to the company itself. You get the proxy materials. You can vote on the board. You can evaluate management’s track record and decide for yourself whether they’ve earned your continued support. You’re not just a participant riding the market’s overall direction. You’re the owner of a specific business, with all the rights that come with it.

For people who enjoy digging into a company’s fundamentals and following it over the years, that’s a meaningfully different kind of investing experience, and the voting rights, even if they’re not the headline reason to do it, are a useful reminder that a stock represents a real business and not just a ticker bouncing around on a screen.

A Balanced Approach

Most investors don’t actually need to pick a side here. A lot of people build their portfolio around a core of low-cost ETFs for broad exposure, then hold a smaller number of individual stocks in companies they’ve researched and want to stay closer to. That combination lets you capture the diversification benefits of pooled investing while keeping a direct ownership stake, and a vote, in the businesses you care most about. There’s no universally correct ratio. It depends on how much time you want to spend, how much you enjoy the research, and what you’re trying to get out of your portfolio in the first place.

The Bottom Line

ETF investing has been a genuine net positive for ordinary investors. It has lowered costs, widened access, and allowed millions of people to build diversified portfolios without needing a finance degree. But that convenience comes bundled with a tradeoff most people never examine closely: when you buy the fund, you generally hand off your seat at the table along with it.

The good news is that this is no longer a fixed, take-it-or-leave-it arrangement. The largest fund managers are slowly building ways for you to reclaim a piece of that vote if you want it, and it’s worth at least checking whether your own funds already offer that option. The smaller, more durable lesson is just to know the deal you’re making. Ownership has always been about more than collecting returns. It’s also about having a voice in how the businesses you own are run. And when enough people decide that voice isn’t worth using, somebody else ends up using it for them, whether or not that’s what they would have chosen themselves.

Sources

- Bebchuk, Lucian A. and Hirst, Scott. “The Specter of the Giant Three.” Boston University Law Review, 2019.

- Bebchuk, Lucian A. and Hirst, Scott. “Big Three Power, and Why It Matters.” Boston University School of Law working paper.

- Boston University School of Law. “Should Index Funds Step Up Their Corporate Governance Game?”

- Vanguard. “What’s ahead for Vanguard Investor Choice in 2026?” and “A new way to participate in Vanguard Investor Choice.”

- BlackRock. “Empowering investors through Voting Choice.”

- Cooley LLP. “Key Updates in BlackRock’s and Vanguard’s 2026 US Proxy Voting Guidelines.”

Be First to Comment